Gowri Shankar Balasubramaniam

Gowri Shankar BalasubramaniamBusinesses in Europe are facing greater risk from fraud. As newer forms of fraud emerge, merchants have to stay ahead of hackers else risk being disrupted. In fact, within the first few months of the crisis starting, global phishing attacks shot up by a whopping 667%.

Jose Augustine

Jose AugustineThe travel industry has been put through its paces in these pandemic times. But with new learnings, smart tech, and resilience it is possible to win hearts and a winning edge again.

Marco Runge

Marco RungeOpen Finance promises to change the way consumers and businesses in Europe use financial services. But what does it mean for you?

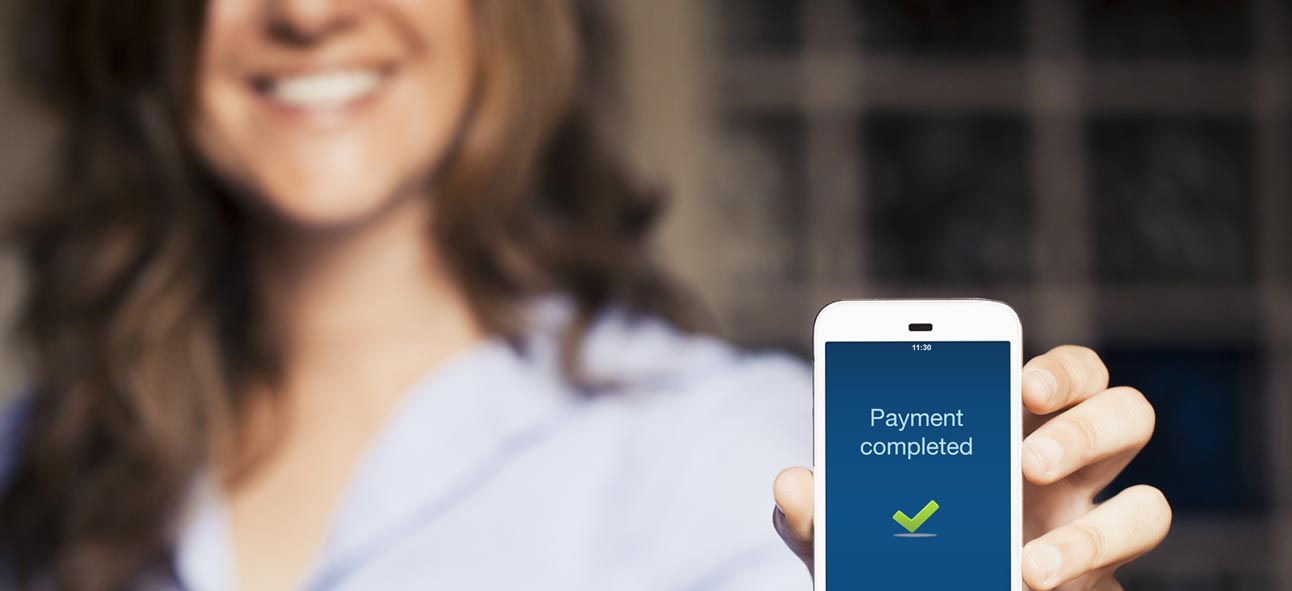

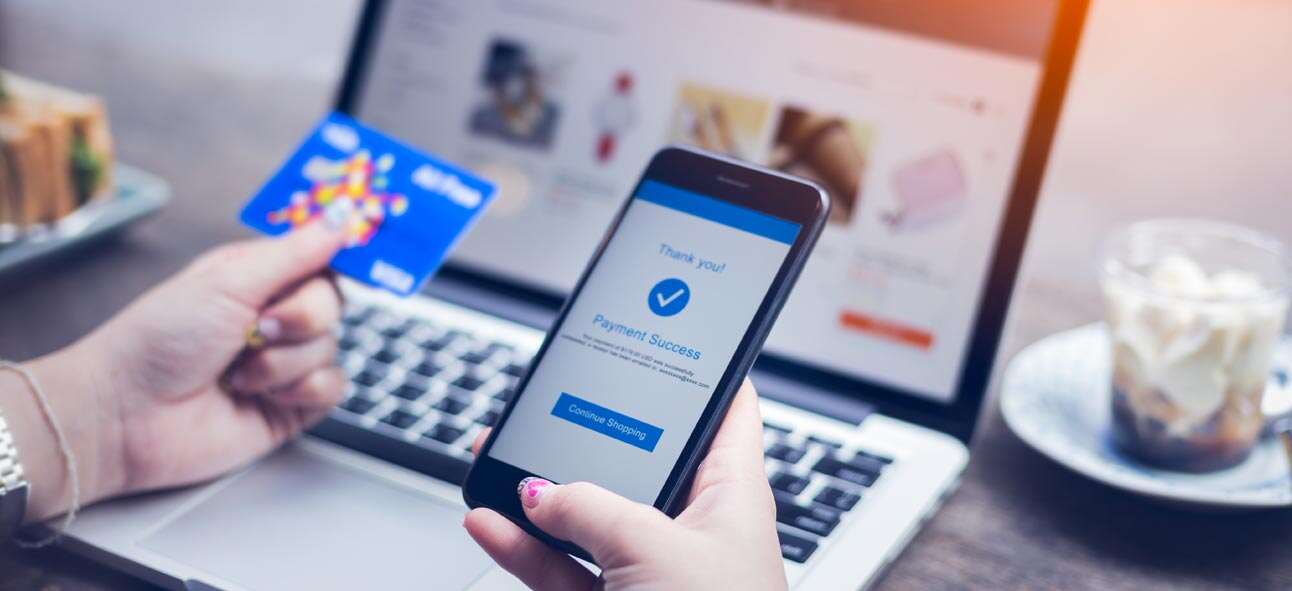

Customers do not like declined transactions. It is a waste of time and effort, not to mention the frustration and anxiety about possible fraud. And when this happens more than once, customers abandon their shopping carts, leading to lost sales. Hence, it should be every business’s priority to enable customers to complete their purchase on the very first try.

With Brexit a reality now, the business landscape across UK and EU is evolving fast. From revised VAT laws, customs duties, to cross-border checks and overall process changes, new rules are coming into play in cross-border commerce between the UK and EU.

Antony Robinson

Antony RobinsonThe widespread emphasis on dynamic flexibility and interconnected solutions for a post-COVID economic resurgence is indicative of digitalization’s strong influence on global decision making, as well as, its value building abilities in the face of a global challenge. And contactless payment solutions are an important indicator of this.

Reducing payment declines is critical in creating a smoother checkout process, improving sales and creating customer delight. Visual appeal, functionality, and security are crucial touchpoints that businesses have to look at in order to boost payment acceptance.

New laws to counter fraud are coming into effect in the EU. Understand how this impacts your business and your customers

Contactless, ‘one-touch’, instant payments are on the rise. And as consumers move towards alternative payments systems that offer more safety and control, the need for greater interoperability in payments systems is spurring new innovation and regulation in the industry.

In July 2020, the maximum limit for instant payment transactions will be raised from € 15,000 to € 100,000. This is expected to increase acceptance of real-time transfers and is expected to drive the development of the associated infrastructure.

In February, traders were able to breathe a sigh of relief: the Federal Court of Justice limited liability to platforms. There were also other interesting legal news relating to trademark law and data protection.

Partner with us

We’ll always have requirements we could fill for each other, whether you are a technology provider, financial services provider, design agency or a business and marketing expert. Apart from enterprise-level partnerships, our referral programs will help build a very attractive long-term passive income stream for SMEs.

Explore partner opportunitiesSubscribe

Never miss a new integration, plugin release or critical industry news.